A VAT (value added tax) with no other tax — no income, corporate, estate, etc. etc. etc. — is pretty much the economists’ ideal. But how do you make it progressive? A bright — or perhaps lunatic— idea occurred to me.

A progressive VAT

Everyone pays the maximum VAT rate — 40% say, equal to the maximum marginal federal income tax rate. Then, as you spend money over the year, you turn in your receipts — figuratively, we’re going to do al this electronically in a second. So, for the first (say) $10,000 of purchases in each year, you get a refund of all VAT taxes paid. For the next $20,000 of purchases, you get $30 out of every $40 tax payments back, so you pay a 10% rate. And so on. Finally, after (say) $400,000 you don’t get anything back, so you pay the 40% maximum rate.

As you see, I give people an incentive to declare all their consumption. That incentive completes one of the main advantages of a VAT over an income or sales tax. In a VAT, each business in the production chain pays the VAT on its inputs, and charges the VAT on its sales. It then deducts the VAT payments on its inputs against the VAT it has to pay on its sales. That gives the business a strong incentive to collect the VAT on sales, and for its business customers to demand proof the VAT was paid so they in turn can deduct VAT payments against their VAT collections. Now people will also demand “receipts,” proof of tax payment.

Clearly this works only if everything is electronic. I would not inflict expense reimbursement drudgery on the American taxpayer. But that largely is the case. We have a sales tax reporting mechanism, so adding or substituting VAT tax reporting is not that hard.

Wednesday, April 26, 2017

Tuesday, April 25, 2017

Long Run Lira?

Luigi Zingales inaugurated a series of essays in Il Sole 24 Ore, an Italian newspaper, on whether Italy should stay in or get out of the Euro, and graciously asked me to contribute. My view, here in English, here in Italian.

To be clear, I kept to Luigi's terms of the debate. This piece is only about whether Italy is better off in the long run, with a common currency. Whether it gets anything out of an exit, a devaluation, a default now is for another day. And this is just about currency, not about leaving the EU, not about debt or austerity, not about whether europe needs a fiscal union, or the rest of it. (Some subsequent correspondence verifies the wisdom, but also the difficulty, of talking about one thing at a time.)

Return to the Lira? A long-run view (Not very good English title)

The euro isn't perfect, but it isn't bad. (Much better Italian title)

Should Italy have her own currency, and run her own monetary policy? For today, let's focus on the long-run question, leaving out for now the transition and any immediate benefits and costs. When contemplating a divorce, it is wise to focus on what life will be like when everything is settled, not just who will have to wash today's stack of dirty dishes.

Remember first that monetary policy cannot substantially improve long-run growth. Long-run growth comes from people and productivity, how much each person can produce per hour of work. In turn, productivity comes from innovation, new companies, new ways doing business, and new products. Like Uber, consumers benefit and existing producers are disrupted. Improvements in long-run growth come only from structural reform, not monetary machination. Money is like oil in a car. Bad monetary policy, like too little oil, can drag an economy down. But after a point more oil will not help you to go faster — you need a bigger engine.

To be clear, I kept to Luigi's terms of the debate. This piece is only about whether Italy is better off in the long run, with a common currency. Whether it gets anything out of an exit, a devaluation, a default now is for another day. And this is just about currency, not about leaving the EU, not about debt or austerity, not about whether europe needs a fiscal union, or the rest of it. (Some subsequent correspondence verifies the wisdom, but also the difficulty, of talking about one thing at a time.)

Return to the Lira? A long-run view (Not very good English title)

The euro isn't perfect, but it isn't bad. (Much better Italian title)

Should Italy have her own currency, and run her own monetary policy? For today, let's focus on the long-run question, leaving out for now the transition and any immediate benefits and costs. When contemplating a divorce, it is wise to focus on what life will be like when everything is settled, not just who will have to wash today's stack of dirty dishes.

Remember first that monetary policy cannot substantially improve long-run growth. Long-run growth comes from people and productivity, how much each person can produce per hour of work. In turn, productivity comes from innovation, new companies, new ways doing business, and new products. Like Uber, consumers benefit and existing producers are disrupted. Improvements in long-run growth come only from structural reform, not monetary machination. Money is like oil in a car. Bad monetary policy, like too little oil, can drag an economy down. But after a point more oil will not help you to go faster — you need a bigger engine.

Monday, April 24, 2017

Inflating our troubles away?

These are comments I gave on

"Inflating away the public debt? An empirical assessment" by Jens Hilscher, Alon Aviv, and Ricardo Reis at the Becker-Friedman Institute

Government Debt: Constraints and Choices conference, April 22 2017, along with generic comments on the conference in general. This post contains mathjax equations.

Long Term Debt

Consider the government debt valuation equation, which states that the real value of nominal government debt equals the present value of primary surpluses.

My first equation expresses this idea with one-period debt, discounted either by marginal utility or by the ex-post return on government debt.

$$\frac{B_{t-1}}{P_t} = E_t \sum_{j=0}^\infty \beta^j \frac{u'(c_{t+j})}{u'(c_t)} s_{t+j} = E_t \sum_{j=0}^\infty \frac{1}{R_{t,t+j}} s_{t+j}$$

(\( P \) is the price level, \( B \) is the face value of nominal debt coming due at \( t \) , \( s \) are real primary surpluses, \( R \) is the real ex-post return on government debt.)

This paper's question is, to what extent can inflation on the left reduce the value of the debt, and hence needed fiscal surpluses on the right. The answer is, not much.

Long Term Debt

Consider the government debt valuation equation, which states that the real value of nominal government debt equals the present value of primary surpluses.

My first equation expresses this idea with one-period debt, discounted either by marginal utility or by the ex-post return on government debt.

$$\frac{B_{t-1}}{P_t} = E_t \sum_{j=0}^\infty \beta^j \frac{u'(c_{t+j})}{u'(c_t)} s_{t+j} = E_t \sum_{j=0}^\infty \frac{1}{R_{t,t+j}} s_{t+j}$$

(\( P \) is the price level, \( B \) is the face value of nominal debt coming due at \( t \) , \( s \) are real primary surpluses, \( R \) is the real ex-post return on government debt.)

This paper's question is, to what extent can inflation on the left reduce the value of the debt, and hence needed fiscal surpluses on the right. The answer is, not much.

Friday, April 14, 2017

Capital Cause and Effect

Òscar Jordà, Björn Richter, Moritz Schularick, and Alan Taylor wrote a provocative What has bank capital ever done for us? at VoxEu, advertising the underlying paper Bank Capital Redux (NBER, CEPR link here, google if you can't access either of those)

It starts with a blast:

With the facts and regressions,

Wow. Now, (this is a good quiz question for a class), before you click the "more" button: Do the facts justify the conclusion? And if not why not?

It starts with a blast:

"Higher capital ratios are unlikely to prevent a financial crisis."Wow! How do they reach this dramatic conclusion? The post and underlying paper are empirical, collecting a very useful dataset on bank structure across countries and a long period of time. They show, for example, that

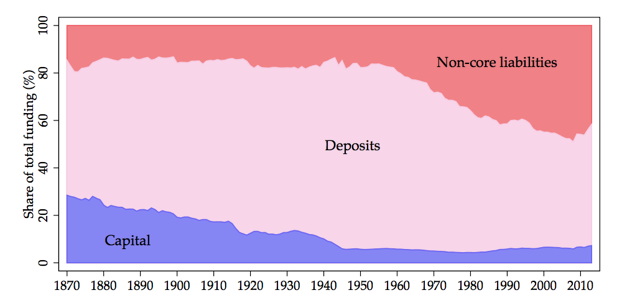

bank leverage rose dramatically between 1870 and the second half of the 20th century. In our sample, the average country’s capital ratio decreased from around 30% capital-to-assets to less than 10% in the post-WW2 period (as shown in Figure 1 below) before fluctuating in a range between 5% and 10% in the past decades.Here is the very nice Figure 1. (It shows not just how capital has declined, but how reliance on more run-prone wholesale funding has increased. The fact that capital used to be 30% is one that we need to reiterate over and over again to the crowd that says 30% capital would bring the world to an end.)

|

We find that the capital ratio provides virtually no information about the probability of a systemic financial crisis.

Whether used singly or along with credit, higher capital ratios are associated, if anything, with a higher probability of a crisis.There used to be a lot more capital, and there used to be a lot more financial crises.

Wow. Now, (this is a good quiz question for a class), before you click the "more" button: Do the facts justify the conclusion? And if not why not?

Wednesday, April 12, 2017

United

Commentators seem to have noticed a lot of the economics of the United fiasco: Yes, don't stop auctions at $800. (WSJ review and outlook.) Yes, if you need employees at Louisville so badly, call up American and buy a first class ticket. Book a private jet. Or, heck, you're an airline. Bring up another plane. Don't drag people off planes to save a measly $500.

The one economic point that I haven't seen: the whole issue also comes down to airlines' use of personalized tickets to price discriminate. (And most of the TSA's job is to enforce that price discrimination by making sure you are the name on the ticket.) If you could resell tickets, the problem would go away. Then the airline must sell only as many tickets as there are seats on the plane, as concerts do. If people aren't going to show, they put their tickets on ebay -- or another quick peer to peer ticket trade platform -- and someone else buys them. Including the airline, if it wants to send employees around. Standby disappears -- want to get on the plane? Bid for a ticket. We still get efficiently full planes -- fuller, even -- nobody ever gets bumped, and the auction for the last seat is going on constantly.

Yes, one of the hardest lessons in economics is that price discrimination can be efficient. Business class cross subsidizes leisure and pays for fixed costs. But the airlines could speculate in their own tickets as well, so its' not clear in a data mining race that scalpers would reap the price discrimination profits better than the airlines themselves.

Holman Jenkins adds, in a brilliant column,

Update: More at the always excellent Marginal Revolution. One negative reaction, already on display at United -- the crush to get on the plane first will increase.

Getting on United vs. Southwest is a study in bad incentives. Southwest: you get a number. People peacefully line up when called, and quickly get on the plane. Southwest also gives free (bundled in the ticket price) bags, so people aren't hauling trunkolads of junk for the overheads. United: Board by groups, and now everyone with a credit card is in group 1. They charge for bags. Midway through the scramble for overhead space, the bins fill up, then people have to start swimming upstream with their huge bags to gate check. If ever there was a way to make an airplane board slower, having people swimming against traffic with huge bags is it. The result, you line up like it's the New Delhi airport (or Southwest, circa 1995) and 100 million dollars of United plane plus crew sits on the ground. I do it too (I'm a rational consumer!) Quite a few times I have had someone show up with a boarding pass with my seat number in it, and being there first makes a big difference. Another fully rational response -- you really want to be a high mileage customer. The love/hate relationship with United will get deeper.

The one economic point that I haven't seen: the whole issue also comes down to airlines' use of personalized tickets to price discriminate. (And most of the TSA's job is to enforce that price discrimination by making sure you are the name on the ticket.) If you could resell tickets, the problem would go away. Then the airline must sell only as many tickets as there are seats on the plane, as concerts do. If people aren't going to show, they put their tickets on ebay -- or another quick peer to peer ticket trade platform -- and someone else buys them. Including the airline, if it wants to send employees around. Standby disappears -- want to get on the plane? Bid for a ticket. We still get efficiently full planes -- fuller, even -- nobody ever gets bumped, and the auction for the last seat is going on constantly.

Yes, one of the hardest lessons in economics is that price discrimination can be efficient. Business class cross subsidizes leisure and pays for fixed costs. But the airlines could speculate in their own tickets as well, so its' not clear in a data mining race that scalpers would reap the price discrimination profits better than the airlines themselves.

Holman Jenkins adds, in a brilliant column,

While we’re at it, what’s wrong with Chicago airport security? Did not a single officer say, “I’m having no part of this. If United can’t deal with its overbooking mistakes in a civilized, non-cheapskate way, how is it my job to manhandle innocent customers?” This also smacks of our national malaise—police who need an armored personnel carrier before they’ll roll up and serve a warrant, who wait outside Columbine High until they’re sure the shooting has stopped.And do not the other passengers rebel at seeing such treatment? Well, maybe not the first time, but I suspect the next time they try to drag a customer off an overbooked plane, there will be a riot.

Update: More at the always excellent Marginal Revolution. One negative reaction, already on display at United -- the crush to get on the plane first will increase.

Getting on United vs. Southwest is a study in bad incentives. Southwest: you get a number. People peacefully line up when called, and quickly get on the plane. Southwest also gives free (bundled in the ticket price) bags, so people aren't hauling trunkolads of junk for the overheads. United: Board by groups, and now everyone with a credit card is in group 1. They charge for bags. Midway through the scramble for overhead space, the bins fill up, then people have to start swimming upstream with their huge bags to gate check. If ever there was a way to make an airplane board slower, having people swimming against traffic with huge bags is it. The result, you line up like it's the New Delhi airport (or Southwest, circa 1995) and 100 million dollars of United plane plus crew sits on the ground. I do it too (I'm a rational consumer!) Quite a few times I have had someone show up with a boarding pass with my seat number in it, and being there first makes a big difference. Another fully rational response -- you really want to be a high mileage customer. The love/hate relationship with United will get deeper.

Wednesday, April 5, 2017

The second original sin of healthcare regulation

Whenever I advance one or another view of how a relatively free health care and insurance market could work a lot better than the mess we have now, the obvious question comes up: Well, what about the homeless person with a heart attack? You won't let him die in the gutter will you?

No. Of course not. We are a compassionate society. We will provide for poor people, very sick people, those with diminished mental capacity, the unfortunate, the incompetent, or the merely improvident. People don't die in the gutter. Any half-reasonable health care reform proposal, including mine, provides some system of charity care; whether via medicaid, government run hospitals (VA for everyone, county hospitals), premium subsidies or vouchers, support for charity hospitals, and so forth; and in our society the government will have a big part in this; I do not appeal to private charity alone. Such systems will also always be a thorn in our public side; as the tension between cost, effectiveness, quality, moral hazard will not magically disappear no matter how nice the promises of their architects, and the fraud, inefficiency, and bureaucracy of anything run by governments will not disappear as well.

But the great puzzle of health care policy: Just why is it, to accommodate this worthy goal, must your and my health care and insurance be so deeply regulated and so thoroughly dysfunctional? As one small example, why does a 20 minute skin check with the resident of my dermatologist generate a phoney baloney bill for over $1000, meaning a cash and carry market for such a simple, elastically demanded, and perfectly predictable service is impossible?

Why, in order to provide for the unfortunate, do we not simply levy taxes, and pay for charity care, and leave the rest of us alone?

No. Of course not. We are a compassionate society. We will provide for poor people, very sick people, those with diminished mental capacity, the unfortunate, the incompetent, or the merely improvident. People don't die in the gutter. Any half-reasonable health care reform proposal, including mine, provides some system of charity care; whether via medicaid, government run hospitals (VA for everyone, county hospitals), premium subsidies or vouchers, support for charity hospitals, and so forth; and in our society the government will have a big part in this; I do not appeal to private charity alone. Such systems will also always be a thorn in our public side; as the tension between cost, effectiveness, quality, moral hazard will not magically disappear no matter how nice the promises of their architects, and the fraud, inefficiency, and bureaucracy of anything run by governments will not disappear as well.

But the great puzzle of health care policy: Just why is it, to accommodate this worthy goal, must your and my health care and insurance be so deeply regulated and so thoroughly dysfunctional? As one small example, why does a 20 minute skin check with the resident of my dermatologist generate a phoney baloney bill for over $1000, meaning a cash and carry market for such a simple, elastically demanded, and perfectly predictable service is impossible?

Why, in order to provide for the unfortunate, do we not simply levy taxes, and pay for charity care, and leave the rest of us alone?

Tuesday, April 4, 2017

Spikes

Jon Hartley, writing in Forbes, offers a great graph of the overnight Federal Funds rate,

This graph mirrors nicely the graph I posted last week, from "Deviations from Covered Interest Rate Parity" by Wenxin Du, Alexander Tepper, and Adrien Verdelhan:

What's going on with these quarter-end spikes?

This graph mirrors nicely the graph I posted last week, from "Deviations from Covered Interest Rate Parity" by Wenxin Du, Alexander Tepper, and Adrien Verdelhan:

What's going on with these quarter-end spikes?

Floating rates?

I was interested to read in the Financial Times, "Iceland weighs plan to peg krona to another currency":

Iceland’s finance minister has admitted it is untenable for the country to maintain its own freely floating currency....Benedikt Johannesson told the Financial Times that the Nordic island of just 330,000 people would look at options to link Iceland’s krona to another currency, most likely the euro or pound.

“Is the status quo untenable? Yes. Everybody agrees on that. We’d like to have a policy that would stabilise the currency. It’s really not good when a currency fluctuates by 10 per cent in the two months since we took over,” said Mr Johannesson, who became finance minister in January.

The main thing is if you want to peg against a currency, do it against a currency where you do business. Once you decide on a currency, that will also change the future. You will do more business with that area,” he added, pointing to Denmark’s experience of doing more business with Germany after pegging its currency first to the Deutschmark and then the euro.

This is interesting in the context of Conventional Wisdom, which says the euro is a bad idea, and every tiny country needs its own currency, to devalue any time there is a "shock." In this view, Iceland is a great success because it did devalue after its banking crisis. I am a skeptic, largely favoring a common standard of value. Greece did not become a growth tiger from its previous umpteen devaluations. I'm interested that even the supposed success story for devaluation does not see it that way.

Update (via marginal revolution) here at Bloomberg. The idea is controversial.

Everyone wants a float after the fact, to devalue their way out of trouble. But everyone should also want a peg before the fact; the firm commitment that you will not devalue your way out of trouble makes international investment and trade flow much better.

Update (via marginal revolution) here at Bloomberg. The idea is controversial.

Everyone wants a float after the fact, to devalue their way out of trouble. But everyone should also want a peg before the fact; the firm commitment that you will not devalue your way out of trouble makes international investment and trade flow much better.

Sunday, April 2, 2017

Consumption vs. GDP

Random Critical Analysis has a really interesting blog post from a while ago, on the difference between consumption and income as measures of well being. The level of data analysis and detail on that blog is really impressive.

The narrow question is whether the US spends "too much" on healthcare. A counterargument has always been, what else should we spend money on? As a society gets wealthier, it's natural to spend more on health care, just as we spend more on art, travel, and so forth.

(The counterargument to that is, whether we spend more or less is beside the point. The point is a dysfunctional regulated oligopoly is charging way too much for what we get. It's not so bad to spend this much, it's bad to get such a bad deal.)

So, the question is not whether the US spends more on health care, the question is whether we spend more on health care relative to a measure of our standard of wealth. Using GDP as a rough proxy, we spend a lot more on health care relative to GDP than other countries.

But, the larger point of the blog post, on which I'll focus -- consumption is not GDP (income). Americans are far better off relative to other countries than we think we are. See the graph:

The narrow question is whether the US spends "too much" on healthcare. A counterargument has always been, what else should we spend money on? As a society gets wealthier, it's natural to spend more on health care, just as we spend more on art, travel, and so forth.

(The counterargument to that is, whether we spend more or less is beside the point. The point is a dysfunctional regulated oligopoly is charging way too much for what we get. It's not so bad to spend this much, it's bad to get such a bad deal.)

So, the question is not whether the US spends more on health care, the question is whether we spend more on health care relative to a measure of our standard of wealth. Using GDP as a rough proxy, we spend a lot more on health care relative to GDP than other countries.

But, the larger point of the blog post, on which I'll focus -- consumption is not GDP (income). Americans are far better off relative to other countries than we think we are. See the graph:

Saturday, April 1, 2017

The Obamacare Unraveling

I usually leave Brad DeLong and Paul Krugman alone. If you haven't figured them out by now, you are beyond my help.

In particular, Brad a few years ago made fun of me for "predicting" in 2013 that Obamacare exchanges would unravel due to adverse selection. I have so far resisted the temptation to needle Brad about that as, well... the Obamacare exchanges unraveled due to adverse selection!

But, unbelievably, Brad is doubling down. While recommending again a snarky 2015 Krugman piece, in which even Krugman was not naming his snarks, DeLong writes:

In particular, Brad a few years ago made fun of me for "predicting" in 2013 that Obamacare exchanges would unravel due to adverse selection. I have so far resisted the temptation to needle Brad about that as, well... the Obamacare exchanges unraveled due to adverse selection!

But, unbelievably, Brad is doubling down. While recommending again a snarky 2015 Krugman piece, in which even Krugman was not naming his snarks, DeLong writes:

Subscribe to:

Posts (Atom)