The latest, "The hare gets rich while you don't: back the passive tortoise" reviews a Nomura report covering the performance of "alternative investments," private equity and hedge funds. (The report is here, alas behind the FT's very confusing paywall.) A while ago I put together a class and talk covering hedge fund literature, but haven't updated it in a few years so reviews with updates are particularly interesting.

The fact that hedge funds and private equity have a lot of beta -- often hidden by infrequent or inaccurate marking to market -- remains true:

|

| Source: Nomura via FT alphaville |

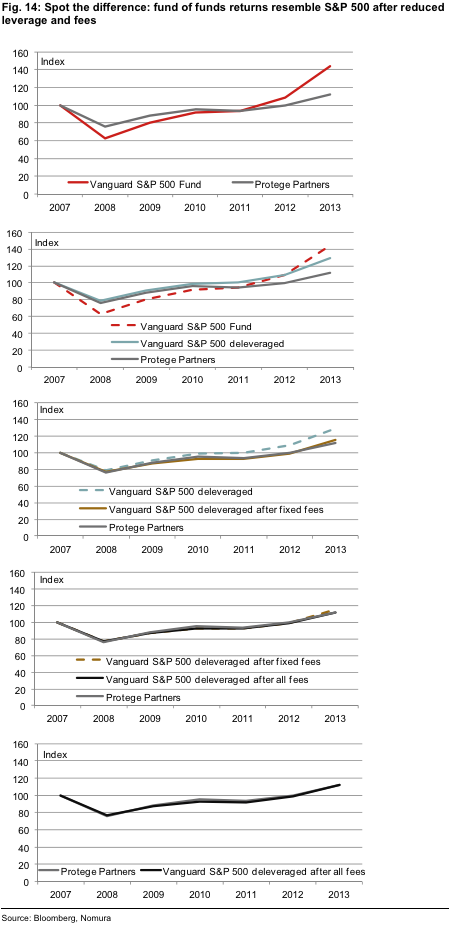

1) start with basic market exposure using the S&P 500 index or a rolling short VIX position,

2) reduce leverage to achieve an exposure of somewhere between 30% to 60% of standard, and

3) deduct fees.

To achieve the returns of private equity:

1) start with a basic market exposure like the S&P 500, but more particularly the S&P Midcap 400, 2) increase leverage to achieve an exposure of somewhere between 120% to 150% of standard, and

3) deduct fees.

Which prompts a game of spot the difference.

Starting with the Vanguard S&P 500 fund, we de-leverage it (to achieve a 57% exposure, which is the beta of Protege Partners to the Vanguard S&P 500) and then deduct both fixed and performance fees. What we are left with is virtually indistinguishable from the performance of the Protege Partners fund of funds."

To me, the private equity results are novel -- though I suspect Steve Kaplan will disagree

I'm interested by their finding that hedge funds do earn just enough alpha before fees to pay their fees. This fits the Berk and Green model in which investors get exactly the same return as in passive investments, more than the Fama and French view that there isn't any alpha in the first place and active investors are just being morons. Extending the Berk Green vs. Fama French debate to hedge fund data is low-hanging dissertation fruit.

Your favorite hedge fund manager will respond, "those results show the average hedge fund doesn't deliver anything to investors. But that's an average of good and bad funds. We're a good fund." Ah, but how to tell good from bad ex-ante, since they all say that? FT reminds us how little past performance tells us with a memorable anecdote:

Day to day, reporting spectacular bets that have paid off for individual hedge fund managers still makes for good stories about the hedge fund industry. But John Paulson did everyone a favour by being the genius of the financial crisis who made several fortunes betting agains mortgage backed securities only to then look like an idiot in 2011 when his flagship fund halved in value.Selection bias is alive and well in private equity, or at least its marketing

To a large extent, private equity promoters are aware that there is some kind of performance problem in their industry. For this reason, marketing documents that we have seen describe the returns investors can achieve in private equity by referring to return data from the top quartile of private equity managers. This is done because the returns from a sample that included all private equity managers would not look impressive.

For the statistically-minded, this practice is a whopper.The rest of the series looks interesting too

Two-thirds of all hedge funds ever to report to a database are dead and defunct, yet their investment record lives on and the industry is hungry for fees...

Dear Professor Cochrane,

ReplyDeleteTo get access to the Nomura report, one needs to be a member of the Long Room, a members-only section of the FT Alphaville. Membership is free of charge and following this link you find all the details http://discussions.ft.com/longroom/faq/.

Kind regrads,

Andreea Mitrache

Dear John,

ReplyDeleteReaders who don't have access to the Journal of Finance can get a nice summary of the Fama/French paper on "Luck vs. Skill" at the Fama/French Forum. The link to that summary is http://www.dimensional.com/famafrench/essays/luck-versus-skill-in-mutual-fund-performance.aspx.

Best,

Jacobo

Thanks.

ReplyDelete"I'm interested by their finding that hedge funds do earn just enough alpha before fees to pay their fees."

ReplyDeleteMaybe I'm making a mistake, but I read the charts differently to you. I thought they suggested that Hedge funds earn negative alpha after fees (hence the black Protege Partners line below the blue 'Vanguard deleveraged' line), and zero alpha before fees (because once they deduct fees in the last panel they almost exactly replicate the Protege Partners returns)?

My brother's financial advisor was trying to sell him a private equity fund. I said don't do it. I'd seen enough to know that they are pretty rough deals, and if they are trying to sell it to doctors in the Midwest, it will be pretty hairy. My other brother who is an executive at a PE owned company agreed with me. We queered the deal. This article confirms my judgement.

ReplyDelete